In her Budget 2025 presentation speech at the Parliament on Saturday (February 1), Finance Minister Nirmala Sitharaman announced that individuals with a salary income of up to Rs 12 lakh will now be eligible for a full income tax rebate under the new tax regime.

This move has been hailed as it provides significant relief to taxpayers by increasing the exemption threshold for income tax under the New Tax Regime from the previous Rs 7 lakh.

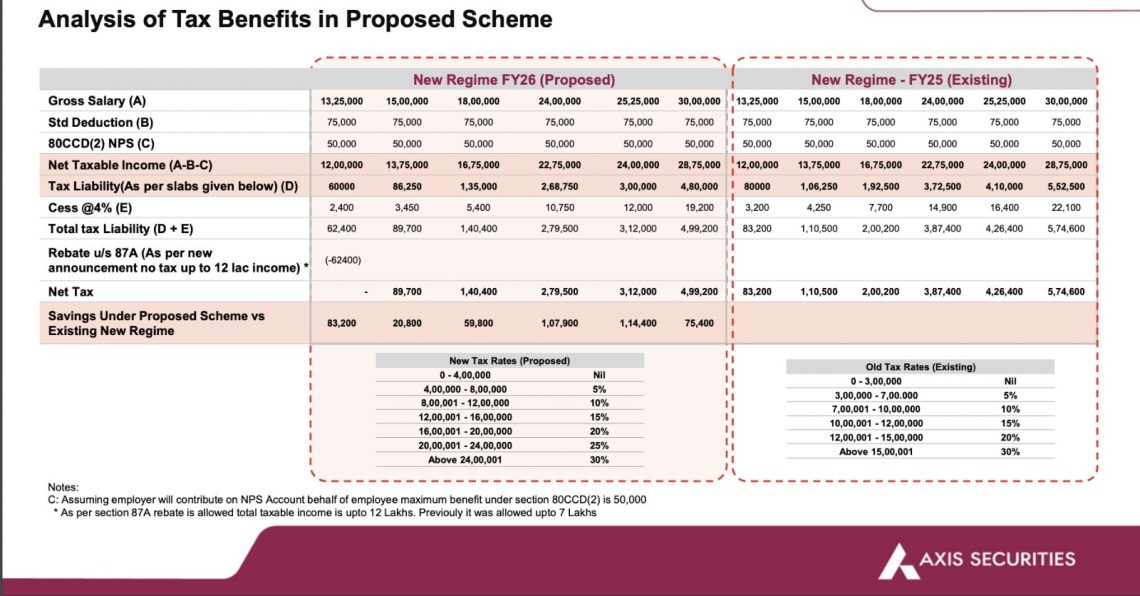

However, the benefits extend beyond those earning Rs 12 lakh.

Individuals with a gross salary income of up to Rs 13.25 lakh can also effectively reduce their taxable income to zero by using available deductions.

Standard deduction: This is a flat deduction allowed by the government to salaried employees and pensioners. It reduces the total taxable income without requiring any bills or proof of expenses and was introduced to simplify the tax filing process and provide relief for expenses like transportation and medical costs.

A standard deduction of a maximum of Rs 75,000 is available to salaried employees, reducing the taxable income directly.

Section 80CCD(2) deduction for NPS: This pertains to the employer’s contribution to the National Pension System (NPS). Employees can claim a deduction of up to 10 per cent of their salary (basic plus dearness allowance) under this section.

For instance, if the basic salary and dearness allowance amount to Rs 5 lakh, the deduction would be Rs 50,000.

By applying these deductions, an individual with a gross salary of Rs 13,25,000 can bring their net taxable income down to Rs 12 lakh, making them eligible for the full tax rebate under Section 87A.

Gross Salary: Rs 13,25,000Less: Standard deduction: upto Rs 75,000Less: NPS contribution (Section 80CCD(2)): upto Rs 50,000Net taxable income: Rs 12,00,000

With a net taxable income of Rs 12 lakh, the individual qualifies for a full rebate under Section 87A, resulting in zero tax liability.

For individuals with higher incomes, the new tax regime still offers substantial tax savings.

There are some caveats, though.

The deduction under Section 80CCD(2) is only applicable if the employer contributes to the NPS on behalf of the employee.

The maximum deduction under Section 80CCD(2) is capped at 10 per cent of the employee’s salary (basic plus dearness allowance) for private-sector employees and 14 per cent for government employees.

Link to article –