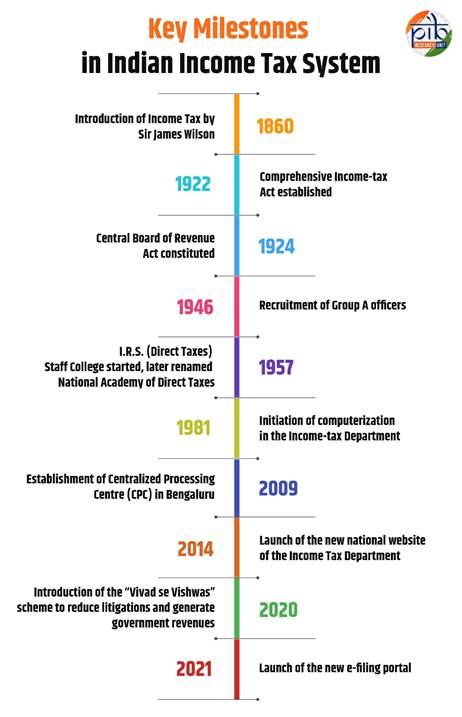

As India marks Income Tax Day 2024, it’s clear that the country’s tax administration has undergone a significant transformation since its humble beginnings in 1860. The evolution from a basic tax system to a modern, tech-driven framework showcases India’s advancement.

The current form of income tax was introduced in India by Sir James Wilson in 1860, two years after the British Crown took the reins of administration in India in its hands following the 1857 War of Independence.

Here are the five things to know about the Income Tax Day:

What is Income Tax?

Income tax is a government levy on the income earned by individuals and businesses during a financial year. “Income” encompasses various sources, defined broadly under Section 2(24) of the Income Tax Act. Here’s a simplified breakdown:

Income from salary: This includes all payments from an employer to an employee, such as basic pay, allowances, commissions, and retirement benefits.

Income from house property: Rental income from residential or commercial properties is taxable.

Income from business or profession: Profits from business or professional activities are taxable after deducting expenses.

Income from capital gains: Profits from selling capital assets like property or jewellery are taxable. These gains can be long-term or short-term.

Income from other sources: This includes income not covered by the other categories, such as savings interest, family pension, gifts, lottery winnings, and investment returns.

This day also highlights the historical development of tax administration in India and the ongoing efforts to enhance tax compliance and simplify the process for taxpayers. The notable increase in personal income tax collections, combined with recent changes introduced in the 2024-25 Budget, demonstrates the government’s dedication to a fair and efficient tax system.

Through improvements in deductions, revisions to tax slabs, and expansion of digital and procedural innovations, the government continues to fortify its approach to taxation. Income Tax Day serves not only as a celebration of India’s fiscal heritage but also as a recognition of the crucial role taxation plays in supporting public services and national development.

As we move forward, the progress made in tax administration and proactive measures to address challenges will undoubtedly contribute to a more robust and equitable economic framework, paving the way for a prosperous and sustainable future.

Income Tax slab in Budget 2024-25:

The Budget for 2024-25 introduced several changes to the income tax regime to benefit salaried employees and pensioners. The standard deduction for salaried employees was increased from ?50,000 to ?75,000 for those opting for the new tax regime.

Similarly, the deduction on family pension for pensioners was enhanced from ?15,000 to ?25,000. Additionally, assessments can now be reopened beyond three years, up to five years from the end of the year of assessment, only if the escaped income is more than ?50 lakh. The revised tax regime provides significant benefits, with salaried employees potentially seeing benefits of up to ?17,500 in income tax.

Link to article –